Advertisement

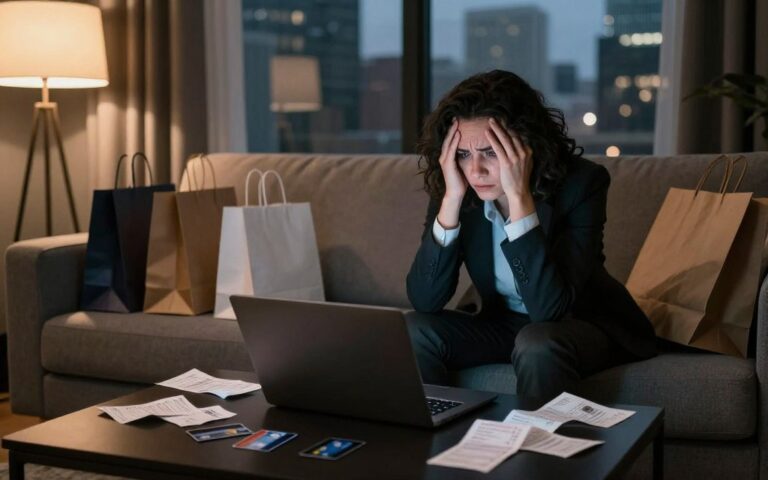

Nearly 40% of Americans say they could not cover a $400 emergency without borrowing or selling something. This shows how common unhealthy money habits have become.

Unhealthy money habits are behaviors or mindsets that quietly harm our progress. They include overspending, ignoring budgets, and avoiding retirement planning. These habits stop good intentions from becoming lasting change.

This article explores 12 common unhealthy money habits. It explains why they matter for U.S. households and offers practical tips. We use data from the Federal Reserve and the Consumer Financial Protection Bureau to highlight the risks.

These risks include reduced savings, higher debt, lower credit scores, and retirement shortfalls. They also lead to more financial stress.

Choose Your Free Shein Content (Tips) to Unlock!

Learn how to get free Shein clothes and items — watch a short ad to unlock your guide.

By clicking “Unlock”, an ad will be shown to release your content.

Each section will define a habit, list clear signs and consequences, and offer strategies. You’ll find budgeting methods, apps, and savings techniques. These tools will help you improve your financial literacy and build healthy routines step by step.

Change doesn’t require perfection. Small, consistent actions are better than quick fixes. Aim to replace one unhealthy habit at a time. Set realistic goals and take practical steps that fit your life.

Understanding Unhealthy Money Habits

First, let’s talk about what unhealthy money habits are. These are actions and attitudes that keep us from reaching our financial goals. Examples include living paycheck to paycheck, buying on impulse, and putting off bill payments.

Definition of Unhealthy Money Habits

Unhealthy money habits happen when we make short-term choices without thinking. This can be spending too much after a bad day or using credit cards for everyday things. It’s often due to stress, confusion, or not knowing where to start.

Common Examples

Many people make the same money mistakes over and over. Surveys show that emotional spending, skipping budgets, and not saving for emergencies are common. These habits can hurt our financial stability over time.

Why They Matter

These habits affect our money in the short and long term. They can lead to late fees and overdrafts, hurting our cash flow. Over time, they can damage our credit scores and make borrowing more expensive.

Long-term, they can mean smaller retirement accounts and fewer chances to build wealth. They also lead to more stress and lower happiness. Studies show that these habits are linked to higher debt and lower savings rates.

Later, we’ll look at specific bad money habits and how to fix them. We’ll share strategies and tools to help you manage your money better.

Emotional Spending Explained

Emotional spending can sneak into anyone’s budget. It links feelings to purchases and fuels many unhealthy money habits. Recognizing the pattern helps you act before small buys become big problems.

Triggers for Emotional Spending

Common triggers include stress, boredom, sadness, celebrations, social comparison, and reward-seeking. Advertising and targeted social media make impulses stronger. One-click checkout and stored cards remove friction and push shoppers toward instant gratification.

Behavioral economics shows dopamine rewards make quick buys feel good in the moment. That rush can override long-term goals and lead to repeating the same unhealthy money habits.

The Impact on Finances

Emotional purchases erode budgets and stall savings goals. Frequent small buys can add up to hundreds of dollars each month. People often rely on credit cards with high interest to cover overspending.

Consequences include higher credit card balances, missed bill payments, and increased buyer’s remorse. Returns and fees can further damage financial progress and make breaking bad money habits harder.

Strategies to Overcome

Use practical rules and tools to curb impulsive behavior. Try a 24- to 48-hour rule for nonessential purchases. Set a discretionary spending limit in your budget. Use cash envelopes or prepaid cards for treat money to create visible spending limits.

Remove stored payment methods from shopping apps and enable friction where possible. Track spending with apps like Mint, YNAB, or Personal Capital to spot patterns and receive alerts about unusual purchases.

Build emotional coping alternatives. Walk, exercise, journal, or call a friend when urges arise. Schedule planned “treat” allowances so rewards don’t trigger binge buying. Seek professional support from a financial coach or a therapist for spending disorders.

Resources from the National Endowment for Financial Education (NEFE) can guide practical money management tips. Combining behavioral changes with tools and support offers the best chance at breaking bad money habits and improving long-term financial health.

Living Beyond One’s Means

Spending more than you earn is a common trap. It starts with small things: a new car lease, upgraded tech each year, dinner out most nights. These choices add up and hide deeper personal finance mistakes that hurt your future plans.

Spotting the problem early helps you avoid financial pitfalls. Below are clear signs to watch for, the consequences that follow, and practical steps to reclaim control.

Signs of Overspending

Relying on credit to cover normal bills is a red flag. Making only minimum credit card payments keeps balances high and interest compounding.

Regular overdrafts or delayed bill payments show cash flow mismatch. Lifestyle inflation — upgrading cars or homes and dining out more as income rises — often indicates values drift from goals.

Consequences for Financial Health

Short-term effects include mounting consumer debt and lower emergency savings. These make unexpected expenses harder to absorb.

Long-term fallout can be worse. Damaged credit scores raise loan costs and slow progress toward homeownership or retirement. Ongoing stress reduces resilience to financial shocks and harms well-being.

Ways to Reassess Spending

Start by calculating true monthly income and separating fixed from variable expenses. Run a 90-day spending audit using bank statements or apps to see where money actually goes.

Sort expenses into “musts,” “wants,” and “savings/debt.” Set targets to bring spending below income. Use the 50/30/20 rule as an initial framework to balance needs, wants, and savings.

Downsize recurring costs by cutting unused subscriptions, comparing insurance, and trimming utilities. Postpone big discretionary buys until you can pay in full. Negotiate bills like internet or cable and use price-comparison tools such as Consumer Reports or marketplace apps when shopping.

Create small, measurable goals tied to values-based spending. For example, shift dining-out savings into an emergency fund for three months, then celebrate the milestone. This approach reduces relapse and makes money management tips practical and habit-forming.

| Step | Action | Expected Result |

|---|---|---|

| 1 | Calculate net monthly income and list fixed vs. variable bills | Clear view of cash flow and ability to set realistic limits |

| 2 | Conduct a 90-day spending audit using bank records or apps | Identify wasteful subscriptions and impulse categories |

| 3 | Classify expenses into musts, wants, savings/debt | Prioritized budget that targets debt reduction and saving |

| 4 | Apply the 50/30/20 rule and set monthly targets | Balanced allocation for essentials, lifestyle, and goals |

| 5 | Negotiate recurring bills and compare prices before buying | Lower ongoing costs and more funds for emergency savings |

| 6 | Adopt values-based spending and celebrate small wins | Stronger habits and reduced chance of repeating personal finance mistakes |

Neglecting a Budget

Ignoring a budget can lead to losing control over money. It makes families more likely to face unexpected expenses. Saving money becomes a challenge. Studies show that tracking spending helps save more and achieve better financial health.

Importance of Budgeting

Budgeting is key to managing finances. It helps plan income, set savings goals, and avoid overspending. It also tracks progress toward financial goals.

Having a budget reduces stress. It shows where every dollar goes. This clarity helps stay on track and avoid debt.

Tools and Apps for Effectiveness

Choose tools that fit your needs. Mint offers free tracking for casual users. YNAB teaches zero-based budgeting for those who want tight control. Personal Capital helps with net worth and retirement planning.

For hands-on methods, try spreadsheets or the envelope system. Use apps with these methods to build lasting habits. These tools help manage money better.

How to Create a Realistic Budget

First, calculate your monthly income. Then, list fixed expenses like rent and utilities. Next, estimate variable costs like groceries and subscriptions.

Set savings and debt targets. Aim for at least 20% savings if possible. Leave some room for discretionary spending to avoid burnout.

Choose a budgeting method that suits you. Zero-based budgeting, the 50/30/20 rule, or pay-yourself-first can work. Review and adjust your budget monthly to account for seasonal changes.

Make budgeting a habit. Automate bill payments and savings transfers. Schedule regular budget reviews to track progress. Use tips and resources to improve your financial literacy and avoid neglecting your budget.

Lack of an Emergency Fund

An unexpected car repair, a sudden job loss, or an urgent medical bill can derail any budget. A clear plan for liquidity helps you stay calm and protects long-term goals. This guide explains what an emergency fund is, how much to save, and simple steps to build one. This way, you can avoid financial pitfalls.

What is an emergency fund?

An emergency fund is a liquid cash reserve for urgent, unplanned expenses. It should be in accessible accounts like savings, checking, or a high-yield savings account. Keep these funds out of stocks or retirement accounts to avoid market volatility.

How much should be saved?

Use essential monthly costs to set a target. This includes housing, utilities, food, insurance, and minimum debt payments. For many Americans, 3–6 months of essential living expenses is a good baseline. If you are self-employed or work in an unstable industry, aim for 6–12 months to better cover income swings.

Steps to build one

Start with a $1,000 mini-fund to cover immediate emergencies. Open a separate FDIC-insured high-yield savings account with banks like Ally, Marcus by Goldman Sachs, or Discover. Automate transfers on payday so saving happens without thinking. Direct tax refunds, bonuses, or other windfalls into the fund until you hit your target.

Trim discretionary spending and use short-term side income to speed progress. Keep emergency savings separate from retirement or investment accounts to reduce temptation. These money management tips lower stress and help you avoid financial pitfalls when life takes an unexpected turn.

| Stage | Target Amount | Where to Keep It | Action Steps |

|---|---|---|---|

| Starter | $1,000 | Checking or high-yield savings | Open separate account, set auto-transfer of small amount each payday |

| Baseline | 3–6 months of essential expenses | FDIC-insured high-yield savings (Ally, Marcus, Discover) | Calculate essential expenses, increase automated savings, redirect bonuses |

| Extended | 6–12 months (self-employed/unstable income) | High-yield savings or short-term CD ladder (liquidity focus) | Use windfalls, trim discretionary spending, consider side income |

| Maintenance | Keep target fully funded | Separate account, FDIC-insured | Review annually, adjust for lifestyle or expense changes |

Ignoring Debt Management

Many people don’t realize how small choices today affect their finances later. Ignoring debt can turn manageable balances into years of stress. This section explains common debt types, the costs of neglect, and strategies to manage debt. It aims to help readers improve their financial literacy and avoid mistakes.

Types of Debt and Their Effects

Credit card debt is revolving and often has high interest. This makes balances grow quickly if only minimums are paid. Student loans come in federal and private forms, with federal loans offering income-driven repayment and forgiveness options.

Auto loans and mortgages are secured by the vehicle or home. This affects the risk of repossession or foreclosure. Personal loans are usually unsecured and may charge higher rates than mortgages.

Secured debt ties to collateral and can have lower rates. Unsecured debt lacks collateral and often costs more. Mortgage interest may be tax deductible for qualifying filers, while credit card interest rarely offers tax benefits.

Terms, rates, and repayment rules shape how each debt affects cash flow and long-term wealth building.

Consequences of Ignoring Debt

Letting balances sit leads to mounting interest costs that outpace principal reduction. Minimum payments frequently cover interest first, so principal falls slowly. Credit scores drop with missed payments, hurting borrowing power and raising future rates.

Long-term neglect can trigger collections, wage garnishments, or lawsuits in extreme cases. Stress and missed opportunities to save for retirement or buy a home are common outcomes. Small debt roles today can delay major life goals tomorrow.

Strategies for Effective Management

Start by listing every account, balance, rate, and minimum payment. This debt inventory is the foundation for change. Choose a repayment approach that fits your psychology and math: the snowball method boosts motivation by closing small accounts first, while the avalanche method saves the most on interest by attacking high-rate debt.

Negotiate with creditors for lower rates or hardship plans when cash is tight. Balance-transfer cards or debt consolidation loans can cut rates if you qualify and follow terms closely. Federal student loan borrowers should review income-driven plans and Public Service Loan Forgiveness rules through Federal Student Aid guidance.

- Automate payments to avoid late marks and reduce stress.

- Build a small emergency fund before accelerating payments, then shift extra cash toward high-priority debts.

- Consider nonprofit counseling from groups like the National Foundation for Credit Counseling for structured plans.

Avoid payday loans and other high-cost borrowing that can trap you in cycles of renewal. Use trusted resources such as the CFPB for consumer guidance. Choosing sound debt management strategies reduces harm from personal finance mistakes and helps improve financial literacy for smarter decisions over time.

Impulse Buying Trends

As digital shopping grows, so does impulse buying. Quick checkout and targeted ads on Instagram and Amazon make it easy to buy on impulse. Without limits, these habits can harm your finances.

Why Impulse Buying Happens

Psychology plays a big role. FOMO and scarcity messaging make us act quickly. Emotional highs after a long day lead to reward purchases that feel good at first.

Technology makes it faster. One-click checkout on Amazon and curated feeds on Instagram reduce barriers. Targeted ads show items when you’re most likely to buy.

Social proof also influences us. Seeing friends post new gadgets or fashion can spark purchases. These can add up quickly.

Effects on Overall Budget

Small purchases can drain your budget. Buying $10–$30 items for convenience or novelty can erode your savings. This can chip away at your discretionary funds.

Credit card balances rise with frequent impulse buys. This increases interest costs and creates a hard-to-break cycle.

Buying too much also leads to clutter and regret. Buyer’s remorse lowers satisfaction. It makes sticking to money management tips harder.

Tips for Controlling Impulse Purchases

Wait before buying. Try a 24–72 hour rule for nonessential items. This pause can help you avoid buying on impulse.

Change your environment. Uninstall shopping apps or log out. Mute promotional emails or use a separate address for deal alerts.

Use tools to enforce limits. Site blockers and budgeting apps can stop late-night browsing. Set spending alerts in your bank app to flag unusual activity.

Adopt concrete controls. Carry cash or use a prepaid card for discretionary spending. Create a monthly “fun” allowance and track impulse spend separately to build awareness.

Pre-commit to a shopping list for essentials. When tempted, check the list first. This habit reduces impulse purchases and helps you follow practical money management tips.

Misunderstanding Credit Scores

Many people see credit scores as mysterious numbers. This misunderstanding can lead to costly mistakes. Knowing how scores work is key to better financial literacy and avoiding credit damage.

Importance of Credit Scores

FICO and VantageScore help lenders make loan decisions and set interest rates. Insurers might use credit data for premiums. Employers and landlords might check credit reports too.

What shapes scores? Payment history (about 35%), how much you owe, and credit use (around 30%). Also, credit history length, new inquiries, and credit mix matter. Knowing these helps improve scores and get better borrowing terms.

Common Myths Debunked

Some think checking their credit hurts it. But soft inquiries don’t lower scores. Closing old accounts can actually harm your score by reducing available credit and shortening history.

Carrying a balance won’t help your score. Paying in full and keeping utilization low is best. Income doesn’t directly affect your score, though lenders consider it for approvals.

How to Improve Credit Health

Start with the basics: pay bills on time and use autopay. Keep credit utilization under 30%, aiming for under 10% for top scores. Avoid opening many accounts at once. Dispute report errors on AnnualCreditReport.com.

Check your reports with Credit Karma or Experian. Use secured credit cards to rebuild history when needed. Changes take time, but responsible actions can raise scores in months. Deeper issues may take years.

Learn from trusted sources like the CFPB and FTC. These guides help improve financial literacy and support long-term credit score improvement. They also help avoid common personal finance mistakes.

Failing to Plan for Retirement

Not planning for retirement can cause a lot of stress. It can lead to needing to save more later, which might cut into your lifestyle. The Social Security Administration says many people don’t have enough to live on in retirement. Start using money management tips and financial education resources now to secure your future.

Why retirement planning matters

Starting to save early can make a big difference. Saving a little each month at 25 can grow more than saving a lot at 45. Waiting to start saving means you’ll need to save more later, which might mean spending less.

Healthcare and long-term care can quickly use up your savings. Medicare doesn’t cover everything. You need to plan for these costs along with your investments and tax-advantaged accounts.

Common pitfalls to avoid

- Not capturing an employer match in a 401(k) or 403(b), which wastes free money.

- Underestimating retirement expenses, like housing, travel, and medical bills.

- Relying on a single asset class instead of diversifying across stocks and bonds.

- Cashing out 401(k) balances when changing jobs and triggering taxes and penalties.

- Procrastination and failing to use catch-up contributions if 50 or older.

Steps towards effective planning

Start saving early and set up automatic contributions. At least match the employer’s contribution. Use IRAs—traditional or Roth—when they fit your tax situation. Increase contributions when you get raises through auto-escalation features.

Diversify your investments based on your time horizon and risk tolerance. Use retirement calculators from Vanguard, Fidelity, or T. Rowe Price to set targets. Consider a fiduciary financial advisor for personalized advice or robo-advisors like Betterment or Wealthfront for cost-effective guidance.

Plan for healthcare and long-term care costs. Use tax-advantaged accounts and remember to use catch-up contributions at 50-plus. Combine these steps with practical money management tips and financial education resources.

| Action | Why it Helps | Tools & Providers |

|---|---|---|

| Capture employer match | Immediate return on contributions and faster growth | 401(k) plans through employers, HR departments |

| Open an IRA | Tax-advantaged growth and diversification | Vanguard, Fidelity, Charles Schwab |

| Auto-escalate contributions | Raises savings without monthly decisions | Plan provider settings, payroll options |

| Use retirement calculators | Sets clear savings targets and timelines | Vanguard, Fidelity, T. Rowe Price calculators |

| Plan for healthcare costs | Prevents eroding retirement income | Medicare guidance, long-term care insurance, HSA accounts |

| Seek professional guidance | Personalized strategy, fiduciary duty protects interests | Fiduciary advisors, Betterment, Wealthfront |

Underestimating Savings Needs

Many people underestimate how much they need to save for the future. Small errors in planning can lead to big problems. Knowing the right timelines and accounts can help avoid these issues. Here are some steps to set realistic savings goals and stay on track.

Understanding Different Savings Goals

Short-term goals are for things you need in 1–3 years, like a vacation or a new appliance. Put these in a high-yield savings account for easy access and some interest.

Medium-term goals are for 3–7 years, like buying a car or a down payment on a condo. Use certificates of deposit or Treasury securities for better returns than a basic checking account.

Long-term goals are for more than seven years, like a home, college, or retirement. Use brokerage accounts, 401(k)s, and IRAs to grow your money and fight inflation.

Targeted funds are also useful. Keep an emergency fund in a liquid account. Use sinking funds for insurance, taxes, and repairs to avoid unexpected costs.

How to Calculate Savings Needs

To calculate an emergency fund, multiply your monthly expenses by the number of months you want covered. For example, if your monthly expenses are $3,000 and you want six months, you need $18,000.

For big goals, estimate the total cost and divide by the number of months until your goal. For instance, a $30,000 down payment over five years is $500 per month. Remember to add an inflation buffer for longer plans.

Use calculators from Bankrate and NerdWallet to get a better estimate. Remember to consider taxes when choosing accounts, as tax-advantaged options can change your needs.

Importance of Regular Contributions

Make saving automatic. Set up automatic transfers from your paycheck or bank account. This builds discipline and uses dollar-cost averaging for investments.

Save like it’s a fixed expense. Check your plan every quarter and adjust if your income, expenses, or goals change. Use separate accounts for different goals to stay motivated.

Balance saving with paying off high-interest debt. If you have a credit card with 18% APR, pay that off first. Use these tips to manage your money better and improve your financial literacy.

Over-Relying on Loans

Using borrowed money too much can lead to big problems. Short-term solutions can turn into long-term issues with interest and fees. Learning to spot these dangers and find better options can protect your credit and future.

Dangers of Constant Borrowing

Borrowing too often can cost a lot through high interest and fees. Some lenders, like payday lenders, charge very high rates. Missing payments can also hurt your credit score.

Constant borrowing can make you dependent on debt. Even making the minimum payment can take a long time to pay off. This makes it hard to save or invest for the future.

Alternatives to Loans

Look for cheaper options before taking a loan. Credit unions often have better rates than big banks. You can also get help from your employer or local nonprofits for things like housing or medical bills.

Use an emergency fund for real emergencies. Talk to service providers about payment plans when you can’t pay on time. Instead of taking on more debt, try short-term jobs to make ends meet. Borrowing from retirement should be a last resort because of penalties and lost growth.

Creating a Debt Reduction Plan

First, list all your debts with their balances, interest rates, and minimum payments. Choose a method to pay off your debt that works for you. The snowball method gives quick wins, while the avalanche method saves money on interest.

Reduce spending on things you don’t need to free up money for your debt. Consider balance transfers or consolidation loans if you can get a better rate. Use budgeting tools to track your progress and stay on track.

If debt feels too much, get help from nonprofits like the National Foundation for Credit Counseling. They offer personalized strategies to manage your debt and avoid financial traps.

| Problem | Short-Term Alternative | Long-Term Move |

|---|---|---|

| Emergency expense | Use emergency fund or gig income | Build 3–6 months savings |

| High-cost payday loan | Negotiate with creditor or seek nonprofit aid | Replace with credit union loan or consolidation |

| Multiple high-rate cards | Balance transfer to lower-rate offer | Consolidate and follow a debt reduction plan |

| Chronic missed payments | Set up payment plan with lender | Use budgeting app and counseling to rebuild |

The Impact of Social Influence

Social forces shape our spending more than we think. Social influence shows up in feeds, friend groups, and event norms. Recognizing these patterns is key to making smart money choices.

Social Media and Consumerism

Instagram, TikTok, and Facebook feeds fuel desire. Influencer marketing and ads push us to buy more. Many buying decisions are influenced by social media, from fashion to travel.

Mute or unfollow accounts that tempt you to spend. This can help lower the urge to buy on impulse.

Peer Pressure and Spending

Peer pressure and spending happen offline too. Dining out and weekend getaways set high standards. Life events like weddings and graduations also raise costs.

Choose when to participate and set limits. This helps avoid debt and buyer’s remorse.

Strategies to Build Financial Independence

Make practical moves to build resilience. Curate your social feeds and set budgets for social activities. Choose low-cost options like potlucks or outdoor meetups.

Practice values-based spending by aligning purchases with long-term plans. Automate savings and use financial education resources. Seek support from peers or a financial coach.

Small, consistent changes lead to steady progress. They help reduce the pull of social influence.

FAQ

What are unhealthy money habits and why do they matter?

Unhealthy money habits are behaviors that hurt your finances. Examples include impulse buying and ignoring budgets. They can lead to less savings, more debt, and stress.Studies from the Federal Reserve and the Consumer Financial Protection Bureau show these habits harm your financial health. They can lead to weaker balance sheets and less money for retirement.

Which unhealthy habits are most common in the U.S.?

Many Americans struggle with emotional spending and living beyond their means. They also neglect budgets and ignore debt. Impulse buying and misunderstanding credit scores are common too.Surveys from Pew Research Center and FINRA reveal many people face these issues. This can make managing money very hard.

How can I spot if I’m emotionally spending?

Look for signs like spending when stressed or bored. Frequent small purchases and buyer’s remorse are red flags. If you spend to feel better but then struggle financially, you might be emotionally spending.

What practical steps stop emotional or impulse purchases?

Try waiting 24–48 hours before buying nonessentials. Set a monthly limit for discretionary spending. Use cash or prepaid cards instead of credit.Apps like Mint and YNAB can help track spending. Find other ways to cope with stress, like exercise or journaling.

How do I know if I’m living beyond my means?

If you use credit for everyday bills, you might be overspending. Frequent overdrafts and delayed payments are also signs. If your spending exceeds your income, you’re living beyond your means.

What’s the fastest way to reassess and reduce overspending?

Start by tracking your spending for 90 days. Categorize your expenses and use the 50/30/20 rule as a guide. Downsize recurring costs and negotiate bills.Set small savings goals and celebrate your progress. This will help you stay on track.

Why is a budget so important—and which tools work best?

A budget helps you manage your money and save. It’s essential for financial control. Tools like Mint and YNAB are popular in the U.S.Some people prefer manual tracking with spreadsheets or envelope systems. Choose what works best for you.

How do I create a realistic budget I’ll stick to?

Start by tallying your monthly income and expenses. Allocate some money for savings and debt. Aim for 20% if possible.Automate your bills and savings. Review your budget monthly and adjust as needed. Simple budgets and automation can help you stay on track.

What is an emergency fund and how much should I save?

An emergency fund is for unexpected expenses. Aim for 3–6 months of living expenses. Start with a $1,000 mini-fund and add to it regularly.Use a high-yield savings account like Ally or Discover. This will help your money grow while you save.

How should I prioritize debt repayment versus saving?

First, build a small emergency fund. Then, focus on high-interest debt while saving a little. Use a debt inventory to choose your strategy.Consider consolidation or balance transfers if they lower your rates. If overwhelmed, seek help from a nonprofit credit counselor.

What are the main types of consumer debt and their risks?

Common debts include credit card, student, auto, mortgage, and personal loans. Risks include high interest, damaged credit, and legal trouble.Payday loans can trap you in debt. Always avoid them. Borrowing from retirement or family should be a last resort.

How does credit utilization affect my credit score and what’s a good target?

Credit utilization is about 30% of your FICO score. Keep it under 30%, and ideally under 10%, for the best scores. Paying off balances and increasing available credit can help.

Are common credit myths true—like checking my own credit hurts my score?

No. Soft inquiries, like checking your own credit, don’t hurt your score. Other myths debunked include carrying a balance and closing old accounts.Income is not a factor in credit scores. These myths can confuse you and harm your finances.

How much should I be saving for retirement and how do I get started?

Start saving early to benefit from compound interest. Aim for 10–15% of your income, adjusting for age and goals. Use 401(k) or 403(b) plans and take advantage of employer matches.Consider IRAs and retirement calculators from Vanguard or Fidelity. A fiduciary advisor or robo-advisor like Betterment can offer personalized advice.

How do I calculate savings needs for big goals like a down payment?

Estimate the total cost and pick a timeline. Divide the total by months to find your monthly target. For example, $30,000 over 5 years is $500/month.Factor in inflation for long-term goals. Choose the right savings vehicle based on your goal’s timeline.

What are safer alternatives to constantly relying on loans?

Build an emergency fund and negotiate payment plans. Use community or nonprofit help for temporary needs. Consider side jobs or low-cost lenders like credit unions.Avoid payday and predatory loans. Borrowing from retirement or family should be a last resort.

How does social media affect spending and how can I protect my finances?

Social media can make you want to buy more, creating FOMO. Protect your finances by unfollowing triggers and curating feeds. Set budgets for social activities and choose low-cost options.Join personal finance communities or accountability groups for support. This can help you stay focused on your financial goals.

What free resources can help me improve financial literacy and break bad money habits?

The Consumer Financial Protection Bureau (CFPB) and National Endowment for Financial Education (NEFE) offer valuable resources. The Federal Reserve provides reports on household finance.AnnualCreditReport.com offers free credit checks. Nonprofit counseling from organizations like the National Foundation for Credit Counseling (NFCC) is also available. Apps like Mint and YNAB can provide hands-on help.