Advertisement

Nearly 70% of Americans say money is a big stress, according to the American Psychological Association. This shows how common financial stress has become.

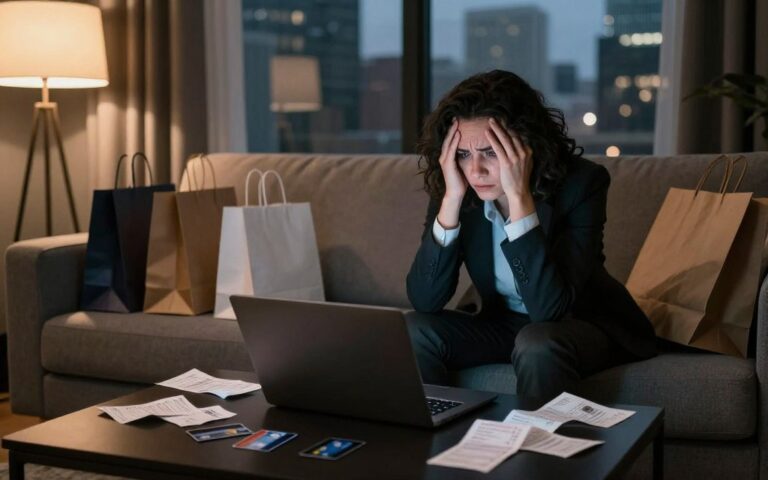

Financial exhaustion is more than a bad month or a missed bill. It’s a long-term state where money, emotions, and health all wear you down. Spotting these signs early helps you avoid losing your health, relationships, or credit.

Rising costs, stagnant wages, and growing debt have put more people under long-term money pressure. The American Psychological Association found links to sleep issues, anxiety, and lower work performance.

This article will guide you in recognizing financial fatigue and burnout. You’ll learn about warning signs, causes, consequences, and steps for support and recovery. Spotting these signs early is key to taking back control and reducing stress from money in your life.

Choose Your Free Shein Content (Tips) to Unlock!

Learn how to get free Shein clothes and items — watch a short ad to unlock your guide.

By clicking “Unlock”, an ad will be shown to release your content.

Understanding Financial Exhaustion

Financial exhaustion grows quietly. Day-to-day money worries pile up until they drain mental and emotional energy. This section breaks down what that looks like, what commonly causes it, and the ways it affects health, work, and relationships.

Defining the Condition

Financial exhaustion is the long-term depletion of emotional and mental resources caused by persistent financial pressure. It’s different from an acute crisis, like sudden job loss or an unexpected medical bill. It’s also different from routine budgeting stress that most people experience from time to time.

Behavioral health research links chronic financial strain to burnout-like symptoms. Constant worry reduces coping ability and decision-making. This pattern makes recognizing financial fatigue important for timely help.

Common Causes of Money Strain

Several drivers push people toward prolonged money stress. Wage stagnation that fails to keep up with inflation leaves many families with shrinking purchasing power. Rising healthcare costs and large medical bills create persistent burdens for those without robust insurance.

Student loan debt and growing credit card balances add long-term pressure. The gig economy and underemployment mean irregular income for more workers. Lack of emergency savings turns one car repair or home fix into a crisis.

U.S. data from the Federal Reserve and the Consumer Financial Protection Bureau highlight average student loan balances and mounting credit card debt as clear contributors to this problem. These factors increase the chances of symptoms of money stress emerging over time.

Impact Across Life Domains

Financial exhaustion affects multiple parts of life. Mental health can worsen, with rising anxiety and depression related to ongoing money worries. Physical symptoms appear, such as disrupted sleep and frequent headaches.

Work performance suffers through reduced productivity and higher absenteeism. Relationships feel strain as conflicts over money increase and social withdrawal follows. Over the long term, savings erode and credit scores suffer, making recovery harder.

Studies show links between financial strain and poorer health outcomes, along with lower workplace engagement. Spotting the warning signs of financial exhaustion early can help people seek solutions before problems deepen.

Recognizing the Warning Signs

Spotting financial trouble early is key for families and individuals. Look for changes in savings, cash flow, and daily spending. These signs often show up before debt gets out of hand.

Sudden decline in savings

Fast use of emergency funds is a big warning. If you’re using savings for regular bills, it means you’re spending more than you make. Experts say to keep three to six months’ worth of living costs saved. Using retirement funds early or dipping below that savings level is a sign to pay attention.

Constant cash flow problems

Often running out of money between paychecks is a sign of trouble. Overdrafts, payday loans, and changing payment dates are signs too. Look for bounced checks, late fees, and juggling bills; these are signs you need to check your budget or income.

Struggles with basic expenses

When it’s hard to pay for basics, your finances are strained. Trouble with rent, utilities, food, transport, or meds is a warning. Using programs like SNAP or Medicaid can help, but needing them long-term might mean bigger issues.

Having to choose which bills to pay is a clear sign of burnout. Catching these signs early lets you take steps like reviewing your budget, finding community help, or talking to a financial advisor.

Emotional and Mental Health Indicators

Financial stress affects our minds before it shows up in our wallets. Recognizing early signs helps us deal with financial stress better.

Anxiety that Centers on Money

Worrying about bills can take over. Thoughts about missed payments or unexpected expenses can interrupt work, sleep, or family time. The American Psychological Association says money is a big stress for Americans. This explains why it’s hard to focus and do daily tasks.

Short Temper and Rising Frustration

Money worries can make us short-tempered. We might get angry at coworkers, partners, or kids over small things. This irritability can hurt our job performance and relationships.

Deep Feelings of Hopelessness

Feeling hopeless about the future can make us lose motivation to manage money. Thoughts like “I’ll never get out of debt” show a hopeless view. These thoughts can lead to depression. Getting mental health support along with financial planning can help.

| Emotional Indicator | Common Signs | Practical Next Step |

|---|---|---|

| Anxiety about bills | Racing thoughts, poor focus, sleepless nights | Track expenses for two weeks; share concerns with a trusted friend |

| Irritability and short temper | Snapping at others, reduced tolerance for delays | Take brief pauses before reacting; set small stress breaks at work |

| Hopelessness and withdrawal | Giving up on budgeting, avoiding future planning | Schedule one meeting with a financial counselor; seek therapy support |

Noticing these signs is key to recognizing financial fatigue. Small steps can help us cope with financial stress when it feels too much.

Changes in Spending Behavior

Changes in spending can show deeper issues. Small choices add up and affect our budgets and happiness. Catching these changes early helps manage money worries and signs of burnout.

Impulsive Purchases

Spending on impulse is a quick fix for stress. A coffee, new shoes, or subscriptions can offer relief. But, these costs add up and hurt our finances over time.

Stress at work, relationship issues, or feeling left out can lead to these purchases. While they feel good at first, they can lead to financial burnout if they outspend our income.

Avoidance of Necessary Expenses

Delaying bills or medical care is a common coping strategy. People might skip car maintenance, dental visits, or insurance payments to avoid financial stress.

These delays can lead to higher costs later, like repair bills or emergency medical care. This shows how spending changes can worsen money problems and stress.

Reliance on Credit Cards

Using credit for essentials is a warning sign when balances grow and cards near limits. Making only minimum payments can trap you in debt with growing interest.

Heavy credit use can hide immediate financial issues but increases long-term debt. This reliance is linked to managing money anxiety and early signs of burnout.

| Behavior | Common Causes | Short-Term Effect | Long-Term Risk |

|---|---|---|---|

| Impulsive Purchases | Stress, social triggers, boredom | Temporary mood lift | Reduced savings, overspending |

| Avoidance of Necessary Expenses | Anxiety about bills, denial | Lower immediate outflow | Higher repair/medical costs, service interruptions |

| Reliance on Credit Cards | Income gaps, emergencies | Maintains daily cash flow | Rising debt, interest traps |

Relationship Strain Due to Finances

Money troubles can affect how families talk and act together. Small arguments over bills can grow into big fights. Spotting early signs of financial stress can help couples avoid resentment.

Conflicts Over Money Issues

Money fights often start from different spending habits, secret debts, or uneven financial contributions. Saving-focused partners might disagree with those who spend more. Studies show money conflicts are a top reason for divorce and unhappy relationships.

Hidden debts or loans can feel like a betrayal. Repeated arguments about who pays for what can erode trust. Couples who manage their money together tend to have less conflict and clearer goals.

Social Withdrawal

Shame about money can make people skip social events. Missing out on gatherings can lead to less support from friends and family. This isolation can make financial stress worse.

Steering clear of social events means fewer chances for advice and support. Simple outings can become a source of worry if a couple feels they can’t afford them. Over time, friends may start to drift away, leaving fewer people to turn to in hard times.

Changes in Family Dynamics

Financial stress can change family roles. One partner might work extra hours or take on a second job. Children may take on more chores or emotional tasks than they should.

These changes can affect family stress and child well-being. Kids who see constant money worries can develop anxiety or take on too much responsibility. Talking about fair roles and financial stress can help families stay stable.

Using clear budgets, setting small goals, and learning to cope with financial stress can ease tension. Counseling, community resources, or financial planning can offer support and reduce relationship strain.

Physical Symptoms of Financial Stress

Money worries can show up in our bodies before we see them in our bank accounts. Recognizing these signs early can help us tackle financial stress. Here’s how financial stress can affect our daily lives.

Fatigue and Exhaustion

Long-term tiredness often comes from constant money worries. People feel drained and struggle with everyday tasks. This is due to poor sleep, long work hours, and constant financial stress.

Changes in Sleep Patterns

Money worries can disrupt sleep. Some can’t fall asleep, while others wake up too early. This can make it hard to focus and make decisions, making money stress worse.

Unexplained Health Problems

Financial stress can lead to headaches, stomach issues, and high blood pressure. It can weaken our immune system and increase doctor visits. These health problems can lead to higher healthcare costs over time.

Small changes like better diet, a simple sleep routine, and financial counseling can help. Spotting these symptoms early can help us overcome financial fatigue and regain our energy.

The Role of Debt in Financial Exhaustion

Debt often sits at the center of financial exhaustion. Rising balances, missed payments, and high interest can erode savings and peace of mind. Recognizing financial exhaustion signs early makes it easier to choose a healthier path.

Growing Debt Levels

Household debt in the United States includes mortgages, auto loans, student loans, and credit card balances. Federal Reserve data shows mortgage and student loan portions make up large shares of total household debt. When balances climb faster than income, resilience drops and stress rises.

Difficulty Making Minimum Payments

Making only minimum payments extends repayment by years. Interest compounds and the principal shrinks slowly. This pattern creates a loop of worry and helplessness that matches common financial exhaustion signs. The psychological toll comes from never feeling ahead and watching debt linger.

Impact of High-Interest Loans

Payday loans, title loans, and high-rate credit cards accelerate balance growth. Predatory terms and triple-digit APRs push borrowers into repeat borrowing. Tracking APRs and comparing offers helps people spot traps. Credit unions, community banks, and nonprofit programs often have lower-rate alternatives that ease pressure.

Practical coping with financial stress begins with a clear picture of obligations. List debts by interest rate and balance. Explore consolidation, credit union loans, or local assistance when needed. Small steps reduce interest costs and restore control.

Long-Term Consequences of Financial Exhaustion

Money troubles can change your life plans and force tough choices. Knowing the long-term effects of financial exhaustion helps you see signs early. This way, you can manage money worries before they cause lasting damage.

Erosion of Savings

Using emergency funds and retirement accounts for daily needs hurts your future. Tapping into a 401(k) or IRA can lead to penalties and taxes. This can delay big goals like buying a home or saving for college.

Small withdrawals add up quickly. Each one chips away at your long-term goals. This pattern is a clear sign of financial burnout, making every financial decision stressful.

Decreased Credit Score

Missing payments, collections, and high credit use harm your credit score. Lower scores mean higher interest rates and limited loan approvals. This creates a cycle of worsening financial strain.

Recovering takes time. A late payment can stay on your report for seven years. But, making on-time payments can slowly improve your score. Checking your reports and disputing errors helps speed up this process.

Potential for Bankruptcy

Bankruptcy can offer relief when debts are too much. But, it has long-term effects on your credit and access to financial products. Chapter 7 wipes out qualifying debt but may require selling assets. Chapter 13 sets a repayment plan to protect property.

Eligibility for bankruptcy depends on income and assets. But, there are better options for avoiding bankruptcy. Debt management plans, negotiating with creditors, and settlement programs can reduce debt without harming your credit like bankruptcy does.

| Consequence | Typical Causes | Short-Term Impact | Long-Term Effect | Possible Remedies |

|---|---|---|---|---|

| Erosion of Savings | Using savings for bills, emergencies, or loan payments | Reduced buffer, increased stress | Delayed retirement, lost investment growth | Build small automatic transfers, cut discretionary spending |

| Decreased Credit Score | Late payments, high utilization, collections | Higher interest rates, loan denials | Costlier credit, housing challenges | Pay on time, lower balances, monitor Equifax/Experian/TransUnion |

| Potential for Bankruptcy | Unmanageable unsecured debt, job loss, medical bills | Immediate debt relief options | Long-term credit impact, limited lending access | Explore debt management plans, negotiate settlements, consult a trustee |

Recognizing financial burnout early makes it easier to take action. Practical steps include making a budget, seeking help from a credit counselor, and finding realistic repayment plans. This way, you can avoid long-term damage.

Finding Support and Solutions

When you start to feel financially exhausted, it’s time to take action. Getting practical help and steady advice can ease your stress. Here are steps to find short-term relief and long-term stability.

Seeking Financial Counseling

Nonprofit credit counseling agencies like the National Foundation for Credit Counseling offer free or low-cost help. A counselor will look at your income, expenses, and debts. They can help with budgeting, teach you about credit, and create a debt management plan for you.

Certified counselors can also talk to creditors for you. They might get lower interest rates or payment plans. This can make your monthly payments smaller and help you see a clear path forward.

Building a Support System

Talk to people you trust about your money worries. Sharing your struggles can make you feel less alone. Support groups are great for swapping tips and advice.

For couples, having open money talks is key. Use neutral language, set goals together, and take small steps. Regular meetings help keep you both on the same page, even when money is tight.

Utilizing Community Resources

Local programs can offer quick help and stability. Food banks and SNAP can help with groceries. Utility and Medicaid programs can lower your monthly bills and health costs.

Community health centers offer affordable medical care. United Way 2-1-1 can connect you to local services. HUD-approved housing counseling can help avoid eviction or foreclosure.

Combining counseling, personal support, and community resources can help you recover. This mix strengthens your recovery and improves your ability to manage financial stress over time.

Strategies to Mitigate Financial Exhaustion

Financial exhaustion can feel overwhelming. Taking small steps can help you regain control and reduce stress. Start with small, daily changes to manage money anxiety and overcome financial fatigue.

Start with a clear plan. Track your income and expenses for a month to find leaks. Choose one budgeting method and stick to it. Simple routines help you stay on track and see your progress.

Budgeting and Financial Planning

Find a budgeting style that fits your habits. Try zero-based budgeting or the envelope system to assign every dollar a job. Prioritize essentials like rent, utilities, and food. Use apps like Mint or YNAB to track spending and spot trends.

Start building an emergency fund, even if it’s small. Aim for $500 to $1,000 first, then grow it over time. Focus on making small, steady changes. These small wins help reduce worry and manage money anxiety.

Exploring Additional Income Sources

Look for income options that match your skills and schedule. Freelancing, rideshare driving, or part-time remote work can add cash without long-term commitments. Selling unused items at local consignment shops or online frees space and brings quick funds.

Consider taking affordable courses on Coursera or LinkedIn Learning to boost your skills and charge more for your work. Track tax implications for side income and balance hours to avoid burnout. Careful planning increases cash flow while protecting your health.

Setting Realistic Financial Goals

Set SMART targets: specific, measurable, achievable, relevant, and time-bound. Aim to pay off a small debt in six months or save $1,000 in an emergency fund within a year. Break larger goals into monthly milestones to keep motivation high.

Celebrate small wins to sustain momentum. Mark progress with simple rewards that cost little but feel meaningful. This approach reduces shame, supports long-term change, and makes managing financial exhaustion feel manageable.

| Action | Start Time | Tools | Expected Benefit |

|---|---|---|---|

| Zero-based budget | Week 1 | YNAB, spreadsheet | Clear spending plan and reduced impulse buys |

| Starter emergency fund | Ongoing | High-yield savings account | Short-term cushion for surprises |

| Side gig (freelance or rideshare) | Weeks 2–4 | Upwork, Uber, local platforms | Additional income and faster debt payoff |

| Skill upgrade course | 1–3 months | Coursera, LinkedIn Learning | Higher earning potential |

| SMART goal for debt | Set immediately | Planner or budgeting app | Motivation and measurable progress |

When to Seek Professional Help

If money worries keep you up at night or affect your work and relationships, it’s time to act. Look out for signs like too much debt, missed payments, or thoughts of harming yourself because of money. If you feel unsafe, call crisis hotlines or a mental health expert right away.

There are many professionals to help with money issues. A Certified Financial Planner (CFP) can guide you on long-term plans and investments. An Accredited Financial Counselor (AFC) specializes in budgeting and managing debt.

For legal help with money problems, see a bankruptcy attorney. For tax issues, a CPA or enrolled agent is your best bet. If money is tight, consider free or low-cost services like nonprofit credit counseling.

Financial coaching offers hands-on help to improve your money habits. Coaches help you stay on track, create plans, and learn better money skills. This can lead to better budgeting, less stress, and progress toward your goals.

When money worries hurt your mental health, combining coaching with therapy can help. This approach can lead to stronger, more lasting results.

FAQ

What is financial exhaustion and how is it different from normal money worries?

Financial exhaustion is a long-term feeling of being drained from constant money worries. It’s not just about worrying about bills or short-term cash flow issues. It’s like chronic stress or burnout.It shows in many ways, like ongoing anxiety, disrupted sleep, and using credit too much. It also means savings are dwindling. This is different from a quick fix that solves the problem fast.

What common causes lead to financial exhaustion in the U.S.?

Several things contribute to it. Stagnant wages and rising costs are big factors. So are growing debts, medical bills, and unstable jobs.High healthcare costs, expensive housing, and not having enough savings also play a part. Data from the Federal Reserve and Bureau of Labor Statistics show how these issues affect many Americans.

What are early warning signs that I’m experiencing financial burnout?

Look out for signs like savings disappearing fast, cash-flow problems, and overdrafts. Feeling worried about bills, irritable, or hopeless are also red flags.Behaviorally, spending impulsively, avoiding bills, and relying too much on credit cards are signs of financial exhaustion.

How does money stress affect mental and physical health?

Money worries can lead to anxiety, depression, and trouble concentrating. It can also make you feel helpless.Physically, it can cause fatigue, sleep problems, headaches, and stomach issues. Studies show it can worsen health and increase healthcare use.

Why might I find myself spending impulsively even when I’m low on funds?

Spending impulsively can be a way to cope with stress. It might seem to help in the moment. But it often makes things worse.Identifying what triggers this behavior and finding cheaper ways to relax can help.

When does reliance on credit become a dangerous sign?

It’s dangerous when you use credit for essentials or only make minimum payments. High-interest products like payday loans make it harder to recover.

How can financial strain damage relationships and family life?

Money disagreements can lead to conflict and erode trust. It can cause secret debts, unequal contributions, and role changes.Children may feel the stress, leading to household tension. Talking openly and setting goals together can help reduce tension.

What community resources and programs can help when finances are strained?

Useful resources include food banks, SNAP, Medicaid, and community health centers. There are also utility assistance programs and HUD-approved housing counseling.Nonprofit credit counselors, local churches, and community action agencies can offer short-term relief and help stabilize finances.

When should I seek professional financial help, and what types are available?

Seek help if you can’t cover essentials, are overwhelmed by debt, or if money worries affect your safety or mental health. Options include nonprofit credit counseling, accredited financial counselors, and certified financial planners.CPAs can help with tax issues, and bankruptcy attorneys may be needed. Combining financial coaching with mental-health support is often beneficial.

What practical steps can I take immediately to reduce financial exhaustion?

Start with a simple budget and track spending. Prioritize essentials and build a small emergency fund. Use tools like Mint or YNAB if helpful.Negotiate bills and call creditors for hardship options. Explore side income cautiously and set small, achievable goals. Small wins can reduce stress and build momentum.

How does growing debt and making only minimum payments worsen the situation?

Paying only minimums extends repayment timelines and increases interest costs. This keeps balances high and makes progress seem impossible. It can also lead to borrowing more.Tracking APRs, consolidating debt, and working with a credit counselor can help break this cycle.

What long-term consequences should I be aware of if financial exhaustion continues?

Long-term effects include losing emergency and retirement savings. Damaged credit scores from missed payments or collections can also occur. This may lead to needing bankruptcy.These outcomes reduce borrowing options, increase costs for mortgages or auto loans, and can delay major life goals.

Are there signs that I need mental-health support in addition to financial help?

Yes. Seek mental-health support if money stress leads to persistent hopelessness, loss of motivation, or withdrawal. Contact crisis hotlines or a mental-health professional if safety is a concern.Financial counseling and therapy often work best together when stress affects wellbeing.

How can I discuss finances with a partner without causing more conflict?

Use neutral language and focus on shared goals. Schedule regular money talks with clear agendas. Start with facts like income, debts, and essential expenses.Set small, achievable steps. Consider joint budgeting tools and, if needed, enlist a neutral third party like a financial counselor to mediate.

What alternatives exist to payday loans and other high-interest options?

Alternatives include credit union loans, small personal loans from community banks, and nonprofit lender programs. Employer hardship funds, local assistance programs, or short-term help from family are also options.A nonprofit credit counselor can negotiate better terms with creditors or suggest manageable debt plans.