Advertisement

About 70% of Americans see buying a home as a key part of the American dream. For many, applying for a mortgage is the first step towards making this dream a reality. The mortgage application process can be complex and overwhelming. But, understanding the home loan process and what to expect can make all the difference.

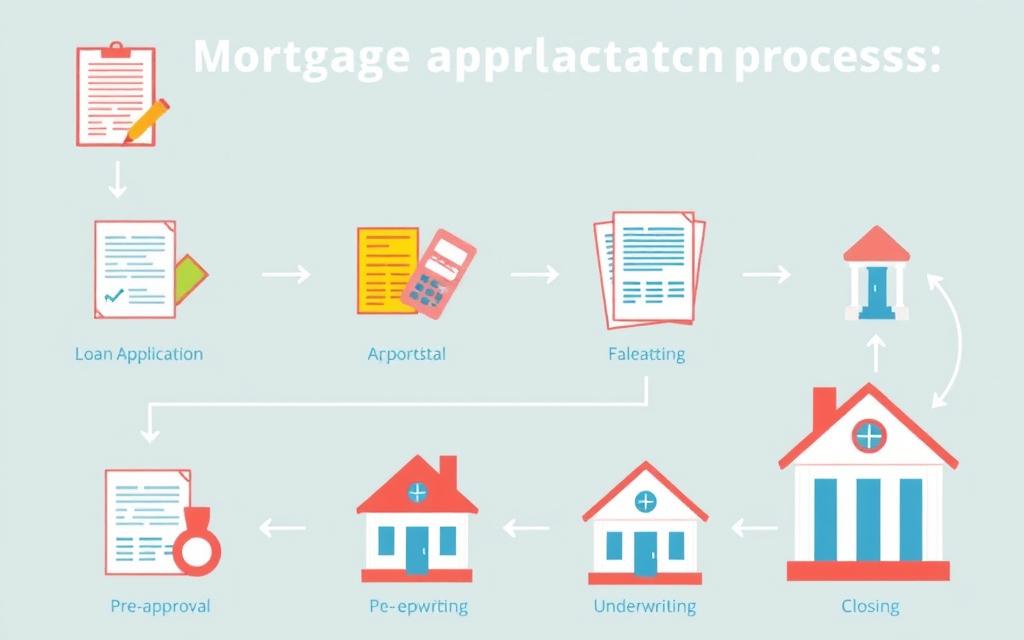

The mortgage application process involves several key steps, from initial application to closing. By grasping the basics of the mortgage application and the various stages involved in applying for a mortgage, individuals can better navigate the process and make informed decisions. This guide will walk you through the entire process, providing valuable insights and expert advice on the mortgage application, home loan process, and what to expect when applying for a mortgage.

Understanding the Mortgage Application Process

The mortgage application process might seem scary at first. But, breaking it down into simple steps makes it easier. It’s a formal request for a loan to buy a home. You need to share personal and financial details with the lender. They then check if you can afford the loan.

What is a Mortgage Application?

A mortgage application asks for your personal info, proof of income, credit history, and details about the property. These are key parts of the process. They help the lender see if you can pay back the loan. Knowing what’s in a mortgage application helps you get ready.

Key Components of a Mortgage Application

The main parts of a mortgage application are:

- Personal identification: This includes documents like a driver’s license, passport, or state ID.

- Income verification: This includes pay stubs, W-2 forms, or tax returns.

- Credit history: This includes info from credit reports, which show your credit score.

- Property information: This includes details about the property, like its value and location.

These parts are crucial in the approval process. Make sure you have all the needed documents before applying.

Preparing for Your Home Loan

Applying for a mortgage means checking your finances and setting a budget. You need to know your credit score, debt-to-income ratio, and down payment savings. Being well-prepared helps you succeed in the mortgage application.

Understanding your mortgage application requirements is key. Your credit score, income, debt, and savings matter. Knowing these factors helps you prepare and boosts your approval chances.

Evaluating Your Financial Health

Checking your financial health is crucial for a mortgage. Look at your income, debt, and credit score. Here’s how to do it:

- Check your credit report and score

- Calculate your debt-to-income ratio

- Review your income and expenses

These steps help you understand your finances. You can then make changes to improve your mortgage chances.

Setting a Budget for Your Home Purchase

Creating a budget for your home is essential. Think about the purchase price, closing costs, and ongoing expenses. A realistic budget ensures you can afford your home and avoid financial stress.

Applying for a mortgage needs careful planning. By checking your finances and setting a budget, you boost your approval chances. This makes the mortgage application smoother.

| Factor | Importance | Description |

|---|---|---|

| Credit Score | High | Affects mortgage interest rate and approval |

| Debt-to-Income Ratio | Medium | Affects mortgage approval and interest rate |

| Income | High | Affects mortgage approval and amount |

The Importance of Credit Scores

Understanding credit scores is key when you’re looking at mortgage steps. A good score can get you a better interest rate. But, a bad score might mean a higher rate or even no mortgage at all. So, working on your credit score is very important.

A good mortgage application checklist will tell you how to boost your score. Pay bills on time, cut down on debt, and don’t apply for too much credit. These actions can save you a lot of money over time.

How Credit Scores Affect Mortgage Rates

Credit scores really matter when it comes to mortgage rates. A high score means a lower rate, which means smaller monthly payments. But, a low score can lead to a higher rate, making your payments bigger.

Strategies for Improving Your Credit Score

To better your credit score, try these tips:

- Pay all bills on time

- Reduce your debt and avoid new credit checks

- Check your credit report for mistakes

By using these strategies, you can raise your credit score. This will help you get a better mortgage deal.

Choosing the Right Mortgage Type

When you’re applying for a mortgage, picking the right type is key. There are many options, and knowing the differences is important. This choice can make the home loan process easier.

Lenders look at your credit score, income, and debt when approving a mortgage. You’ll often see two main types: fixed-rate and adjustable-rate mortgages. Fixed-rate mortgages have the same interest rate for the whole loan. Adjustable-rate mortgages can change over time.

Government-backed loans, like FHA, VA, and USDA, offer special benefits. They might have easier credit score rules and lower down payments. Here’s a quick look at what each mortgage type offers:

| Mortgage Type | Interest Rate | Down Payment |

|---|---|---|

| Fixed-Rate Mortgage | Fixed | Typically 20% |

| Adjustable-Rate Mortgage | Adjustable | Typically 20% |

| FHA Loan | Fixed or Adjustable | As low as 3.5% |

| VA Loan | Fixed or Adjustable | No down payment required |

| USDA Loan | Fixed or Adjustable | No down payment required |

Choosing the right mortgage depends on your situation and goals. By understanding the options, you can confidently move through the mortgage application process.

Gathering Necessary Documentation

When you apply for a mortgage, having all your documents ready is key. You’ll need financial documents like pay stubs, bank statements, and tax returns. Having these documents ready can help avoid delays or application rejection.

The mortgage application process involves a lot of paperwork. But being prepared can make a big difference. Required financial documents may change based on the lender and mortgage type. But, they usually include:

- Pay stubs

- Bank statements

- Tax returns

- Identification documents

You’ll also need to provide property details and insurance information. Knowing what documents you need and having them ready is crucial. This ensures a smooth mortgage process and boosts your approval chances.

Additional Information to Prepare

Applicants should also prepare to share more information. This includes your employment history and credit reports. Lenders use this to check your creditworthiness and set mortgage terms. By gathering all necessary documents and information, you can make your mortgage application successful. This is the first step towards owning your dream home.

Pre-Approval vs. Pre-Qualification

Understanding the difference between pre-approval and pre-qualification is key when applying for a mortgage. Pre-qualification gives a rough idea of your borrowing limit. Pre-approval, though, involves a deeper look at your finances and credit, leading to a lender’s conditional offer.

Pre-approval is a big deal in the mortgage world. It shows sellers you’re serious and ready to buy. To get pre-approved, you’ll need to share financial documents like pay stubs and tax returns. The lender will then check your credit and finances to decide how much to lend.

The perks of pre-approval include:

- More power when making an offer on a home

- A clearer view of your budget and mortgage choices

- A better chance in the housing market, as sellers favor pre-approved buyers

Knowing the difference between pre-approval and pre-qualification helps you through the mortgage process. It guides you in making smart choices about your mortgage needs.

Getting pre-approved is a crucial step. It helps you understand your budget and boosts your chances of getting your dream home.

Choosing a Lender

When you’re applying for a mortgage, picking the right lender is key. You have many choices, like banks, credit unions, and mortgage brokers. It’s important to know what each offers. The right lender can make a big difference in your mortgage journey.

Think about these things when choosing a lender:

- Interest rates and fees

- Loan terms and how you’ll pay back the loan

- How well they treat their customers

Looking at these points will help you find a lender that fits your needs. Always ask questions and compare different lenders. This way, you’ll make the best choice for your mortgage application.

By researching and picking the right lender, you can make the mortgage process easier. Take your time to look at all your options. If you need help, don’t be afraid to ask.

Completing the Application

Applying for a mortgage can be done online or in-person. Each method has its own benefits. It’s important to pick the one that fits your needs best. No matter the choice, make sure the application is filled out right and fully.

When applying, you’ll need to share personal and financial details. This includes your income, credit score, and job history. Double-checking this info is key to avoid mistakes that could slow down or even block your application.

Here are some tips to avoid common mistakes in the mortgage application process:

- Verify your personal and financial details for accuracy

- Make sure all necessary documents are included

- Thoroughly review your application before submitting it

By following these tips and understanding the steps, you can boost your chances of a successful application. Take your time and review your application carefully to ensure it’s accurate and complete.

If you need more help with your mortgage application, consider talking to a financial advisor or mortgage expert. They can guide you through the process and help with any questions you have.

| Mortgage Application Method | Advantages |

|---|---|

| Online Application | Convenience, speed, and ease of use |

| In-Person Application | Personal interaction, immediate feedback, and guidance |

The Underwriting Process

The underwriting process is key in the mortgage application. It’s where the lender checks if they can trust the borrower. A detailed mortgage application checklist is vital. It makes sure all needed documents are in order, making the mortgage processing steps smoother.

The lender looks over the application, credit report, and other papers to decide on the loan. How long this takes can change. It depends on the application’s complexity and the lender’s speed.

What Happens During Underwriting?

The underwriter checks the borrower’s income, job, and credit score. They also look at the property’s value and condition. This step can take a few days to a few weeks, based on the lender and the application’s details.

How Long Does Underwriting Take?

Underwriting usually takes 2-4 weeks. But, it can take longer sometimes. Knowing what happens during underwriting and how long it takes can ease worries. A well-organized mortgage application checklist and efficient mortgage processing steps can speed things up.

Closing the Mortgage Loan

The final step in getting a mortgage is closing the loan. This means signing the loan papers and transferring the property’s ownership. It’s key to know the mortgage application needs and how to get a mortgage to do this well.

At closing, you’ll look over and sign the loan papers, pay closing costs, and get the property keys. Closing costs include things like title insurance and appraisal fees. Knowing these costs helps you manage your money better.

Steps Involved in Closing

- Reviewing and signing the loan documents

- Paying closing costs

- Receiving the keys to the property

- Transferring the ownership of the property

Understanding Closing Costs

Closing costs change based on where you are and the property type. It’s important to include these costs in your budget when applying for a mortgage. Knowing the mortgage application needs and steps helps you feel confident during closing.

Make sure to read all documents carefully and ask questions if you’re not sure. With the right knowledge and preparation, you can close your mortgage loan and start your new life as a homeowner.

Post-Closing Responsibilities

After closing on a mortgage, homeowners have many ongoing duties. The first is making the first mortgage payment on time. This sets the stage for the whole loan period. It’s also key to understand and meet other homeownership duties like property upkeep, tax payments, and insurance.

Making Your First Payment

Making the first mortgage payment on time shows you’re financially responsible. It also helps build a good credit history. Homeowners should know the payment schedule, how to pay, and any late fees or penalties. This ensures payments are made correctly and on time.

Understanding Homeownership Obligations

Keeping the property in good shape, paying property taxes, and having the right insurance are crucial. Regular maintenance and repairs keep the home’s value up and make it safe and comfortable. Also, paying taxes on time and having the right insurance can prevent big penalties or unexpected costs.

FAQ

What is a mortgage application?

A mortgage application is a formal request for a loan to buy a home. You provide personal and financial details to the lender. They then check if you’re creditworthy.

What are the key components of a mortgage application?

The main parts of a mortgage application are personal info, income proof, credit history, and property details. Each part is crucial for the lender’s decision.

How do credit scores affect mortgage rates?

Credit scores greatly influence your mortgage rate. Better scores mean lower rates, while lower scores can lead to higher rates or denial.

What strategies can I use to improve my credit score?

To boost your credit score, pay bills on time, reduce debt, and avoid new credit checks. Improving your score can save you thousands over the loan’s life.

What is the difference between pre-approval and pre-qualification?

Pre-qualification gives an estimate of your borrowing capacity. Pre-approval, though, involves a detailed review of your credit and finances, leading to a conditional loan offer.

What types of mortgage lenders are available?

There are banks, credit unions, and mortgage brokers. Each has its own benefits and drawbacks. It’s important to compare and ask questions to find the right lender for you.

What happens during the underwriting process?

The underwriting phase is when the lender evaluates the risk of lending to you. They review your application, credit report, and other documents to decide on the loan.

What are the steps involved in closing the mortgage loan?

Closing the mortgage loan involves reviewing and signing documents, paying closing costs, and getting the property keys. Knowing the closing process and costs is key for a smooth transition to homeownership.

What are my post-closing responsibilities as a new homeowner?

As a new homeowner, you must make timely payments, maintain the property, pay taxes, and manage insurance. Understanding these duties is crucial for property value and avoiding legal or financial problems.